Caledonia Mining: Isabella-McCays-Bubi gold project looks risky (NYSE: CMCL)

chonticha wat

Introduction

In January 2021, I wrote an SA article about Zimbabwe-focused gold miner Caledonia Mining Corporation Plc (NYSE: CMCL) in which I said the company would have been interested in mothballing Isabella-McCays-Bubi gold project in northwestern Zimbabwe.

Well, a deal was signed in July 2022 and Caledonia is paying $53.3 million in shares for the company owning the project plus a net smelter royalty of 1% on the revenues.

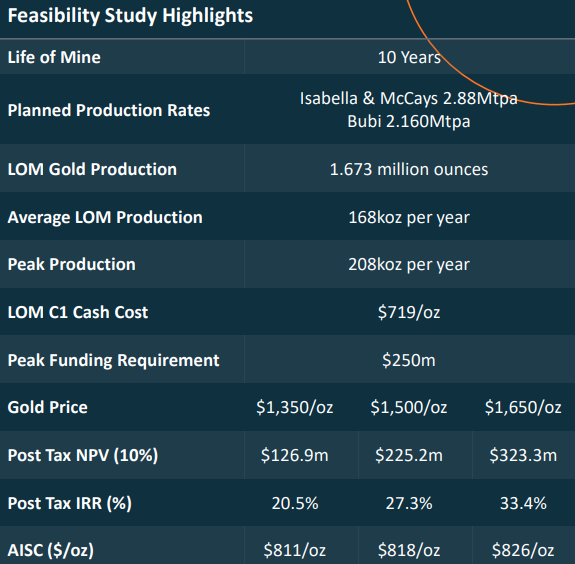

At first glance, this seems like a bargain considering Isabella-McCays-Bubi has a net present value (NPV) of over $300 million. However, the maximum funding requirement is $250 million, which Caledonia does not have, and the ore is mostly sulphide. In my opinion, this is a high risk project that can easily lead to cost overruns and delays. I’m still bearish on Caledonia.

Introducing Isabella-McCays-Bubi

The project is owned by a company called Bilboes Gold and consists of three surface heap leach mines that have produced over 280 koz of gold from oxide ore. However, 235 koz of this amount were produced over a 13-year period ending in 2002 and the average production between 2003 and 2013 was only 4,200 ounces.

DRA

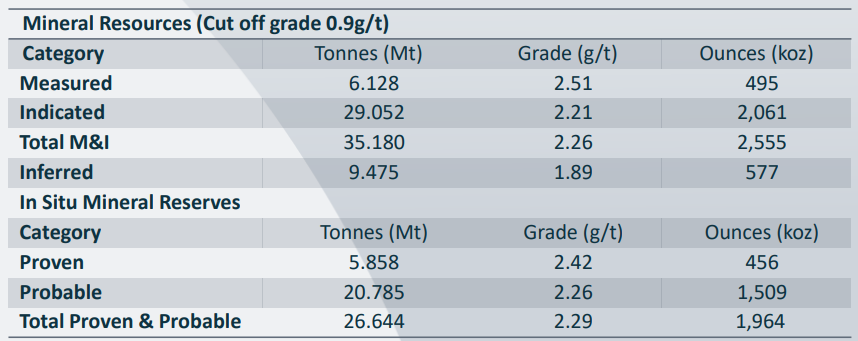

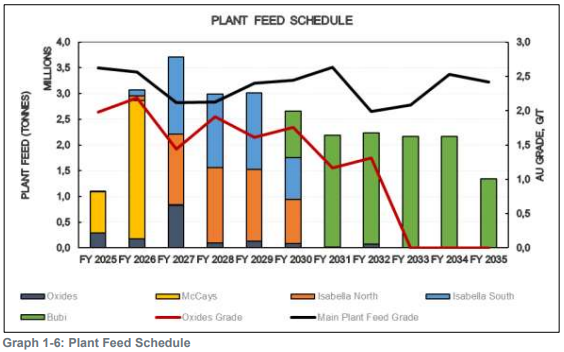

Oxide ore is technically easy to process, so a heap leach is usually a good solution, and the problem here is that Isabella-McCays-Bubi has nearly run out of it. Currently, the project has proven and probable reserves of 1.96 Moz at an average grade of 2.29 g/t, but looking at the mill feed schedule from a study of feasibility of 2020, we can see that oxides represent a small part of the planned production.

Mining Caledonia Mining Caledonia Mining Caledonia

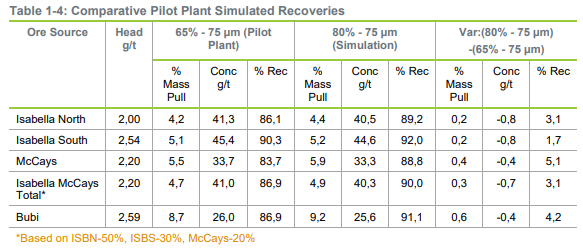

Sulphide ore is difficult to process and miners regularly encounter problems with low recovery rates. Additionally, this type of gold ore usually requires an expensive carbon leach (CIL) plant as well as bio-oxidation (BIOX) for a mine to run well. Looking at the pilot plant recoveries from the feasibility study, the results don’t look great. The DRA engineering group has concluded that approximately 84% of the contained gold can be recovered using BIOX technology with gravity processing and CIL.

Mining Caledonia

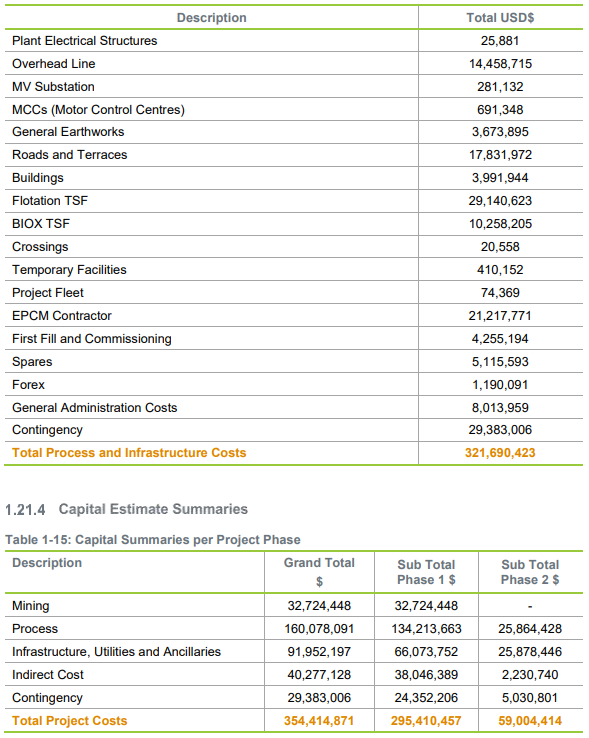

Another problem concerns the initial costs. According to the feasibility study, total process and infrastructure costs are estimated at $321.7 million, while total project costs are expected to be $354.4 million. The maximum funding is $250 million.

Mining Caledonia

That’s a lot of money for a miner of Caledonia’s caliber, so the company wants to take a phased approach to development. The company estimates that starting with a production of around 60 koz would reduce the peak initial capital investment to less than $100 million. However, I see two problems here. First, I can’t think of a single mining project developed in a phased approach that has worked well from a financial standpoint. Second, Caledonia has a 5.5% dividend yield, which has prevented it from building up a cash reserve of nearly $100 million. In June 2022, the company had cash and cash equivalents of barely $10.9 million. Of course, net cash from operating activities was $26.9 million for the first half of 2022 and attributable net income for the period was $17.2 million, but Blanket Mine reserves are expected to run out in 2026. It appears that significant inventory dilution to fund the development of Isabella-McCays-Bubi is likely.

So what does the project timeline look like? Well, Caledonia wants to conduct its own feasibility study which would take about a year. After that, the company will need to secure financing and there are approximately 11 months of waste stripping to expose enough ore for a constant ore feed rate. If all goes well, Isabella-McCays-Bubi could resume business operations in 2025.

Overall, I think the key financials from the feasibility study look good, but I don’t like the shift to a phased approach and the lack of oxide ore. Additionally, it is a project located in Zimbabwe, which is widely regarded as one of the worst mining jurisdictions in the world due to political and economic instability, power outages and a history of nationalization plans . I think Isabella-McCays-Bubi is a risky project that shouldn’t be worth much right now.

For Blanket, Caledonia’s 64% share of net mine cash flow between 2022 and 2026 is $117.2 million using an average gold price of $1,660. ‘ounce. This means that unless the company cuts its dividend or the price of gold rises in the coming years, significant stock dilution could occur.

That being said, I think shorting Caledonia shares could be dangerous as commodity prices are notoriously volatile and gold is no exception. A spike in gold prices could send the company’s stock soaring.

Takeaway for investors

Caledonia has a relatively small gold mine whose reserves run out in 2026 and it looks like the company is planning to make Isabella-McCays-Bubi its new flagship project within a few years. Seems like a good buy at just 0.16x NPV, but there are important reasons why this property is so cheap. Isabella-McCays-Bubi has high initial investments and there is a lot of sulphide ore, which is technically difficult to process. Additionally, the project is located in Zimbabwe and I find it unsurprising that Bilboes Gold has not been able to find financing for it for years (the definitive feasibility study was published in February 2020).

Even if all goes well, I think there will likely be significant stock dilution here. In my opinion, it might be best for risk-averse investors to avoid Caledonia shares.